July 17, 2022

Weekly Market Outlook

By Keith Schneider

Economic news drives Wall Street especially updated critical data points pertaining to inflation, earnings, and interest rates.

Economic news drives Wall Street especially updated critical data points pertaining to inflation, earnings, and interest rates.

It has been a week of negative news on most of these fronts.

Monday thru Wednesday, the stock market drifted lower on anticipated bad news on inflation. Hawkish rhetoric from a few Federal Reserve Governors exacerbated the situation.

Wednesday morning the latest on CPI was released and rose by 1.3% for June. The numbers also indicated that the CPI was up 9.1% year-over-year. Much hotter than was expected and not seen since the early 1980s. Inflation not only continued to rise in June, but the data was much worse than expected.

The increase was broad based as well. Gasoline, shelter, and food all being the largest contributors to the 9.1% rise for the 12 months. The energy index rose 7.5% over the month and contributed nearly half of all items increase with the gasoline index rising 11.2% after a small 4.1% increase in May. Natural Gas rose 8.2% in June, the largest monthly increase since October 2004. The energy index rose 41.6% over the past year while the gasoline index increased a devastating 59.9%, representing the largest 12 month increase in that index since March 1980. Electricity rose 13.7% the largest 12-month increase since the period ending April 2006.

The need for the Fed to get more hawkish immediately hit the market. Many economists were hoping (and expecting) that recent data showing a slowdown would prompt the Federal Reserve to hike at their upcoming meeting by just 50 bp, after this news hit the preponderance of views was that 75 bp was baked in the cake. Others pointed out that it was time for the Fed to get very aggressive and raise rates by 1.0%. Unprecedented.

While the U.S. Fed at its upcoming meeting will only hike by 75 basis points, it is important to note that the Bank of Canada recently hiked rates by a full 100 basis points (1.0%) and the European Central Bank is set to raise rates for the first time in a decade next week for the first time in a decade.

After falling the past few weeks because of a perceived slowdown in the economy, the 10-year began its rise, yet again. Ending the week at about 3.0% and the 2-year note stretching to 3.13%, this inverted yield curve is predicting a recession sometime in the next year. In the past this has been a reliable indicator. See chart below:

Thursday, JP Morgan and Morgan Stanley both reported significant earnings misses on higher revenue. JP Morgan also announced a halt on their future share buybacks, something Wall Street has not seen in a very long time (remember that there were $800 billion in corporate buybacks during 2021 helping to artificially prop up the stock market).

JP Morgan's CEO, Jamie Dimon was quite negative on the state of the economy and stated the following:

"On the one hand, Dimon said, the U.S. economy continues to grow and both the job market and consumer spending, and their ability to spend, remain healthy. But geopolitical tension, high inflation, waning consumer confidence, the uncertainty about how high rates have to go and the never-before-seen quantitative tightening and their effects on global liquidity.... are very likely to have negative consequences on the global economy sometime down the road," he warned.

The JP Morgan news met with another day of selling in the stock market on Thursday. Negative market action recovered by day's end and the markets ended slightly down and the NASDAQ was up a little. Some recovery.

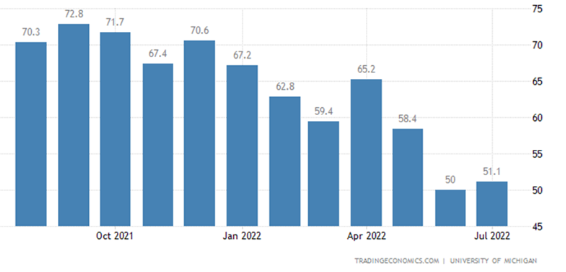

On Friday, the University of Michigan consumer sentiment readings came out better than expected showing a slight improvement over May's awful 50 number. (Please note that the 50% fell from high consumer sentiment numbers of 67.2 in January) Also Citi Bank reported better than expected earnings and the S&P was up better than 2%, the tech heavy NASDAQ was up over 2.5% helping to recover most of the week’s losses. The S&P was down less than 1.0% for the week.

Has inflation subsided and everything is now on better footing?

As we mentioned last week, NOBODY knows. We did see some positive signs over the past few weeks that may imply, even with hot CPI and PPI inflation numbers, we may be seeing the slowdown the Federal Reserve would like to see.

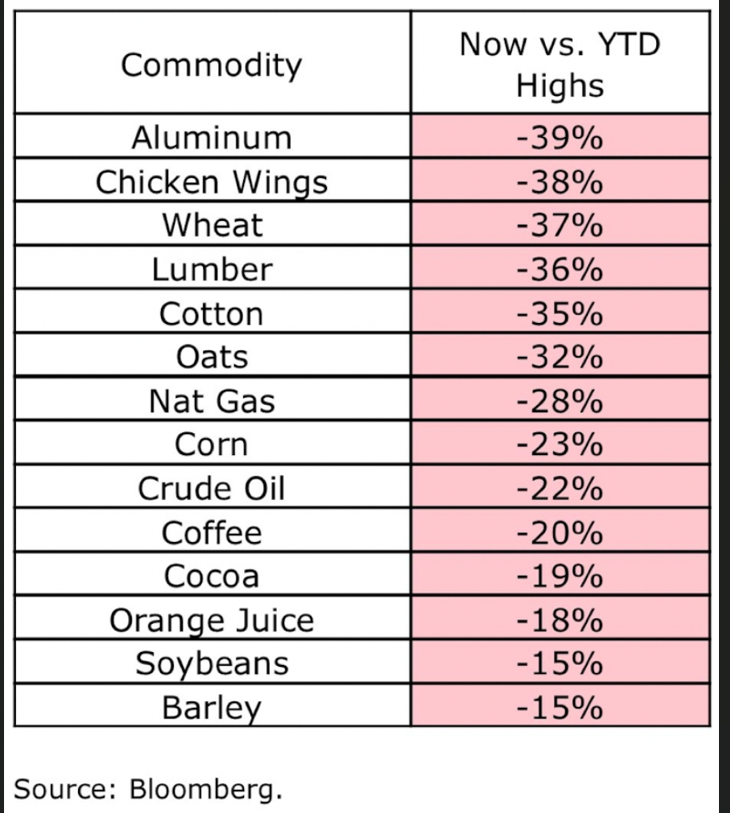

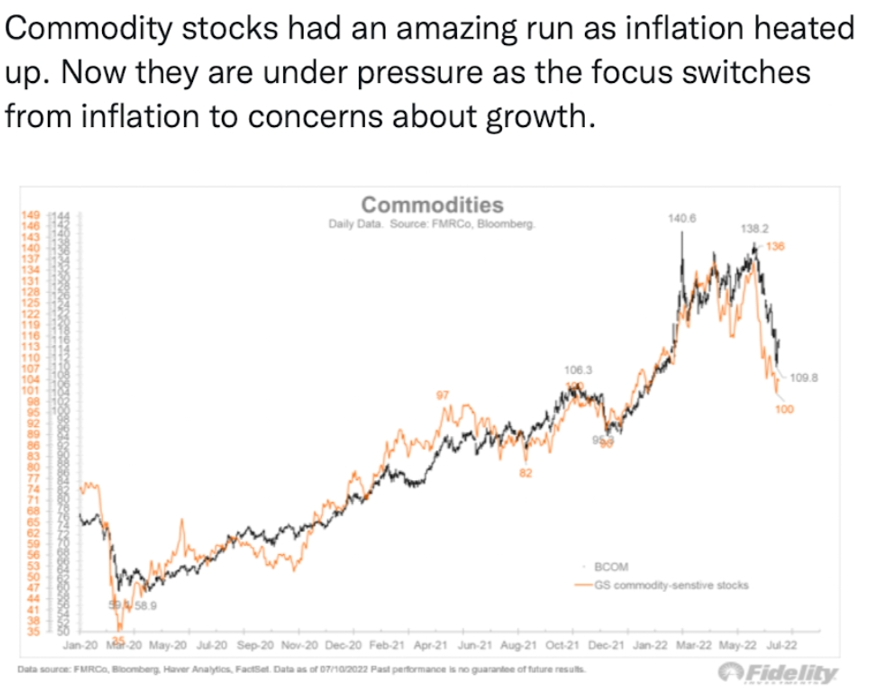

One of the numerous charts we have seen recently include a listing of the change in commodity prices from their highs earlier this year until this past week. This should have a more positive effect on the ongoing inflation narrative IF these are sustainable and we don't see oil or copper, or lumber turn around and head higher in the near future. See charts below:

Add to these fast-changing economic indicators is the fact that the US Dollar has recently hit a new high and gone to parody (equal value) to the Euro. This has not happened for two decades. This nearly 20% rise in the US Dollar over the past 12 months can be attributed to many factors including a flight to quality with many investors sitting in cash.

Whatever the reasons (and there are many), this will add a currency headwind on corporate earnings this year and perhaps even into next year. With many of the US largest companies having between 30-40% of their earnings coming from overseas, this could knock their earnings down substantially due to the punitive damage a stronger dollar does when converting overseas sales to US revenue.

Our own Mish had much to say this past week on a few important appearances. She commented on everything from inflation, earnings, the commodity supercycle we find ourselves in, and other relevant economic indicators. Watch these replays here:

HOW TO STAY ONE STEP AHEAD

As we have pointed out on numerous occasions in previous Market Outlooks, here are some ways you can stay one step ahead:

Market Insights from our Big View service:

Risk On

Risk Off

Neutral

Every week you'll gain actionable insight with: