December 4, 2022

Weekly Market Outlook

By Keith Schneider

As we enter December, it is good to note that we just came off two positive, back-to-back months. This type of action, especially in a midterm election year (of a first term President), suggests that a more profitable and positive stock market may be ahead. Please note a few charts that sum this up:

One of my favorite CMT (Chartered Market Technicians) is Ryan Detrick. He put out a few things this week that give a favorable picture going forward:

And breadth these past two months has been impressive:

However, Inflation Persists

While most of the above information may give investors a sense of renewed optimism, it is important to remember that we remain in an elevated inflationary environment. The Fed has raised rates aggressively in 2022.

This past Wednesday, Chairman Powell said it was likely the Fed could begin to moderate the future rate hikes. The market rallied. It liked the news until Friday at 8:29 am arrived and then…

Came a hot job report. New job creation was well above expectations. The unemployment rate stayed at 3.7% and wage gains climbed to 0.6% well above the market’s expectations of 0.3%.

The strong wage gains in the U.S. November jobs report put out Friday may have just put another 0.75% interest rate hike back on the table for the Federal Reserve’s policy meeting in two weeks.

The market shook off the news. After opening down 1%, the market recovered most of the day’s losses. There is a positive bullish bias right now.

The long bond (which we are invested in through the ETF: TLT) rallied by day’s end and continued the sharp decline of interest rates on the long end. The 10-year rate has now declined from 4.25% in October to 3.5% in six weeks. This, along with the US Dollar’s decline in value has helped push stock prices higher. See chart below of the 10-year yield and the US Dollar (versus the Euro):

After hitting multi year highs in value against the Euro (and other worldwide currencies such as the British Pound, the Japanese Yen, and others) the US Dollar has declined about 15%. This has had a positive effect on stock market valuations as it is perceived to be positive (and additive) to large multinational corporation’s earnings. The S&P 100 companies currently receive over 30% of their revenue (and earnings) from international trade and a weaker US Dollar is beneficial for their future earnings.

Will the Positive Stock and Bond Market Continue?

There is certainly positive momentum right now. However, we remain skeptical given that the Fed will continue raising short-term interest rates and this is bound to cause more volatility and readjustments to earnings. We will continue to monitor (see Big View below) and closely watch the risk gauges, which are cautious at the moment. It is our ongoing adherence to risk management that will help us prevail in this tricky, choppy market. Currently the seasonality factors are providing some tailwinds. (For more information about the seasonality see above and the past few week Market Outlook commentaries, which can be found in the archives, here).

-

The Metals Markets Just Got Shinier

Exactly a month ago, our own Mish “Guru” Schneider appeared on Fox Business News with Charles Payne. You can watch the replay here.

During that segment (and others) Mish reiterated her positive outlook on Gold and Silver. It has remained one of her favorite themes for 2022 (and will be a highlighted theme in her upcoming 2023 Outlook). Readers of Market Outlook will be the among the first to be notified that this valuable annual research report is available. If you’re not receiving Market Outlook via email, register here.

What precipitated her conviction? She has repeatedly stated on National TV that inflation is not ending anytime soon. Stagflation is upon us. She has also suggested that paper assets may be rangebound for some time. If this is anything like the 1970’s, then the markets may traverse sideways for some time.

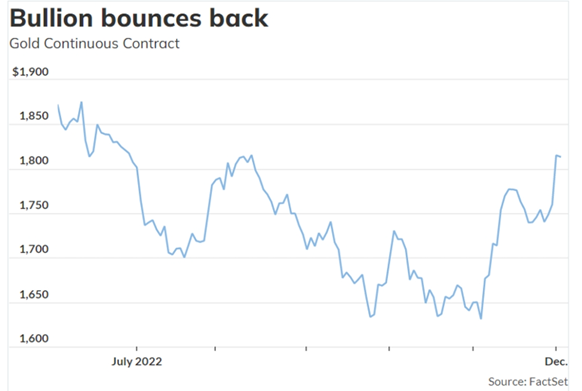

This will benefit nimble traders and active rules-based investing (MarketGauge’s core business). This should also benefit inflationary commodities including the softs (agricultural) and base metals, gold, and silver. The recovery in Gold and Silver may have just started:

Here is most recent action in Silver (Mish has owned GLD and SLV at various times during 2022):

Once Chairman Powell had provided evidence that the Fed would likely moderate their interest rate hikes, the bonds rallied and the dollar fell further, Gold and Silver exploded higher. It was a good week for Gold and Silver. Mish tweeted that she thought a $5,000 per ounce in Gold was in the future.

While you may glean from our thoughts (and bias) motivation to take a sizable position in Gold and Silver, please know that these metals will have many future peaks and valleys (volatility). Especially (and when) the Fed continues to raise rates and we see additional US Dollar strength. So be diligent and don’t get carried away.

Looking back (all that is Gold may not shimmer):

It has been a difficult year. Most money managers and the majority of mutual funds, ETF’s and fixed income strategies are down significantly for 2022 so far (11 months). We are fortunate that we have several strategies up on the year and a few that are down much less than the market. Looking at the holdings that make up these strategies, here are a few of our big winners this year (the numbers cited are for max return before taking profit targets):

*Current position

^Mish’s Premium

The above winning (partial) trades this past year would have been experienced in different MarketGauge strategies. Trades Listed above were found in three different MarketGauge strategies. These strategies have positive performance for 2022, thus far.

If they were part or all of your investment thesis and you blended them together (or we did it for you) this year, you would be profitable. This is the reason we have been encouraging subscribers (and non-subscribers) to invest in combinations or blends using our strategies!

MarketGauge investment strategies exploit different investment edges and are unique. By blending these disparate strategies (some stocks, some ETF’s which include fixed income, commodities, energy, and agricultural ETFs), you get the potential for lower drawdowns (risk) and much better returns than market benchmarks. This would have you outperform the majority of the investing universe of managers and strategies. This is called High Alpha Investing.

If you would like more information on utilizing these blends in your investments, please reach out to Rob Quinn, Chief Strategy Manager at (407) 770-7637, [email protected], or book a call with Rob here. Please also feel free to contact me, Donn Goodman directly at [email protected].

Here is additional detailed information from our Big View:

Risk On

Neutral

Risk Off

Every week you'll gain actionable insight with: