April 1, 2023

Weekly Market Outlook

By Keith Schneider

Happy end of the first quarter Gaugers. The markets (both stock and bond) pleasantly surprised for the month and the quarter.

Are we headed for sunny blue skies and a path to new highs?

Is this a sustainable breakout?

Are these signs that investors should STOP their defensive actions and move aggressively into stocks?

What could derail the positive bias?

Let’s explore a few of these points in further detail:

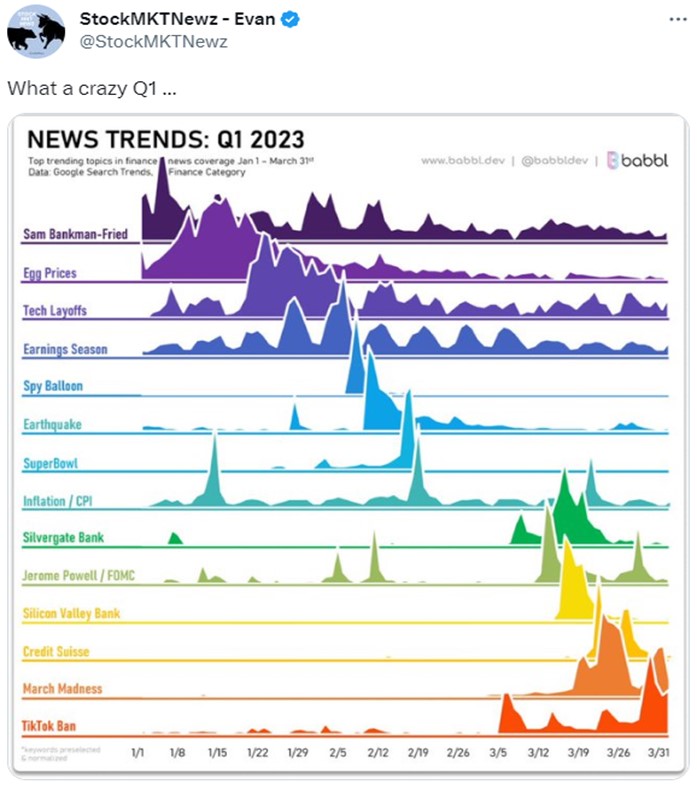

A Month of Unprecedented News (Let’s Review):

What a month… and the stock performance shrugged it off.

Here is a great chart showing all of the 1st quarter news. I include it to show you just how much has been going on these past three months. It has truly been a remarkable, news filled and volatile time:

The Market’s Sharp Turn Mid-Month.

After early month weakness, much of it due to the regional bank crisis and financial stocks selling off, money rotated to big tech. One of the largest swings from weakness to strength we have seen in some time. See charts below:

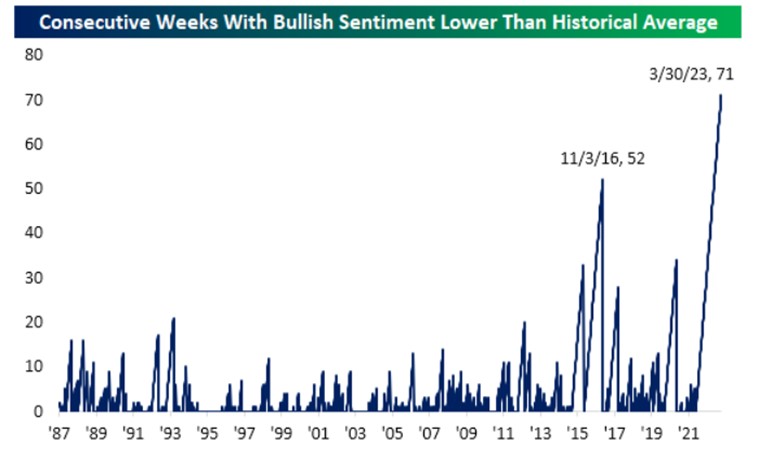

The financial stocks’ sell-off, precipitated by a run on some banks as well as a flight to quality, contributed to bearish sentiment readings. As we have said many times in previous Market Outlooks, when bearish sentiment gets this negative, it actually becomes a contrarian bullish indicator. See graphs below.

This also contributed to investor fear and uncertainty. Money continued its flow to fixed income and interest bearing accounts. March saw record inflow into cash (and outflows from investment portfolios) that surpassed the huge cash that accumulated during the COVID Pandemic. See chart below:

Rangebound

Over a year ago, our own Mish commented on one of her national TV appearances that we would likely see a range bound market along with Stagflation. This has been part of our mantra in these weekly updates (Market Outlooks) in the past. You can see in the chart below the sideways and volatile action of the S&P 500 over the past year.

March was volatile. However, consistent with historical March patterns, the back half of the month was positive. See March progression chart below:

Good U.S. Stocks Performance but International Markets Even Better!

Positive back-to-back quarterly returns since the beginning of the 4th quarter, 2022 bodes well for stocks. But the brightest spot has been international stocks. See graph below:

Two Good Quarters for the S&P 500 May Mean Good Things Going Forward

Historically whenever the S&P 500 has had two good quarters in a row, more gains follow. See chart below:

A Positive Sign. The December Low Indicator

For the month of March, there was a significant diversion between the major indices. The S&P 500 (up 3.3%) and QQQ (up 9.3%) were positive, and the DJIA (-1.1%) and small cap IWM (-5.2%) were negative. However, the December low indicator measures the performance of the first quarter as compared to the December low for the S&P 500 Index.

This has been a reliable indicator and with the S&P 500 up over 7% for the quarter and not violating the December closing low of 3,783, it triggered a bullish signal on the December Low indicator. This indicator was created by Forbes writer Lucien Hooper back in the 1970s. He observed that whenever the market violated its December low within Q1 of the following year, it was an ominous sign for stocks for the remainder of the year. In contrast, if the market holds above the December low as it did this year, it is a bullish sign for the market. See chart below:

As shown in the table above, the December low indicator has an impressive track record. For years when the S&P held above the December low in Q1, the average annual return has been 18.5% with 94% of years finishing positive. When the S&P 500 violated the December low in Q1 the index only generated a modest average annual return of 0.4% with only 53% of years producing a positive return.

However, one Negative: The Soldiers Are Not In Sync With the Generals

As noted above, the small caps (IWM) did not participate in the March rally. Some of this was attributable to smaller regional banks and financial companies being affected by the Regional banking crisis coupled with the Fed raising interest rates that affects small businesses more than larger, cash rich businesses.

One cautionary sign to the “rosy” stock market picture painted above is when small caps do not participate with the large companies. Many analysts believe this portends a weak market, and a future sell-off is certain.

Most of the S&P’s return in the past few months is directly attributable to the largest capitalization companies that contribute the most to the index returns. See chart below:

Here is another chart showing the emphasis the largest technology companies have contributed to the QQQ index.

What Might April Have in Store for Investors?

We have already provided some empirical evidence above that may provide a positive backdrop for the market’s good momentum and possible upside to continue. Many of our technical indicators also support this.

We have gone from Risk Off to Risk On in a short time period. Investor sentiment and many of our inter-market relationships have improved quite dramatically, especially during the past week.

Unlike March, historical progressions for April show a strong first half of the month. During the first 12 trading days, the S&P 500 has historically climbed 1.4%, capturing the majority of the gains for the month. See progression chart below:

April seasonality trends suggest the buying pressure could continue. Since 1950, the S&P has posted average and median April returns of 1.5% and 1.2% respectively. In addition, the index (S&P 500) has finished positive during the month 71% of the time, marking the highest positivity rate on the calendar. These numbers increase in potential probabilities in pre-election years. See graph below:

Here is additional information from our friends at Stock Trader’s Almanac regarding the performance in other indices in pre-election years since 1950. See chart below:

Conclusion

I hope that we have provided a positive but balanced view of the most recent market behavior and what might be expected in the near future. Given the softer inflation data on Friday and the overwhelming belief that the Fed is almost done raising rates, investor sentiment has grown more positive this past week.

Having said that, please be aware of some potential land mines that could derail this scenario. They include:

Have a good week, and be careful out there!!!

Now here is the rest of the story from Keith and our insight from our Big View service:

Risk-On

Risk-Off

Neutral

Every week you'll gain actionable insight with: