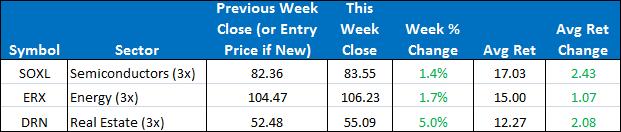

This week we there were no changes to Sector Plus positions. To open next week, we will remain in SOXL, ERX, and DRN.

The SPY closed the week up +0.9%. The ETF model had a good week finding a nice move in DRN to end the week up overall +2.7%. The ETF Sector Plus Strategy is now up +16.47% year-to-date compared to its benchmark, the SPY, which is now up +1.9%.

This Week’s Strategy Lesson: Designing a Strategy

Last week I talked a little about the central concept that we built our ETF strategies around: Relative price momentum and how it relates to trend persistence. This simple concept by itself can be used to give us a strong market edge.

In fact, to demonstrate its power, we created a basic strategy around this concept with a few simple rules. We tracked the six-month percent price change of 11 sector ETFs and ranked them daily. Then we bought the top ETF and held it until it dropped to second place, at which time we would sell out and buy the new top sector ETF.

If you traded this simple strategy over the last seven years (the same period as our backtest in the ETF Sector/Country models), you would be beating the SPY by almost 3-to-1, up 81% versus the SPY up only 31%. I should warn you, though, that this strategy might be hard to follow and with some work, it could be greatly improved upon in a number of ways.

When designing the ETF models, we identified several specific areas where we could potentially improve our model and then systematically went through and tested and analyzed the results. I will go over the first one here and continue through the list over the next couple of weeks.

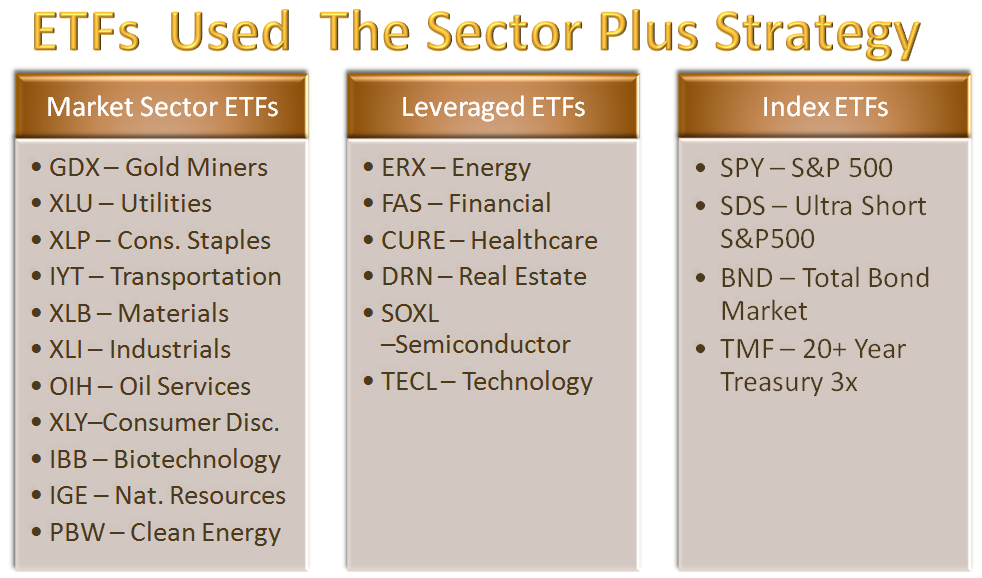

Define/Expand the list of Trading Instruments.

As I mentioned earlier, in the basic model above, I just pulled out 11 of the largest sector ETFs. But there are several areas of consideration that we can use to improve on this selection.

First, we wanted our selection to cover all the “objectives” of our model. As you may know, we now have two ETF models, one focused on sectors and the other focused on countries. One the key objectives for the sector model was to have all the sectors represented so that we can participate in all the rotational phases of the liquidity cycle. This is more of a fixed list representing a closed system.

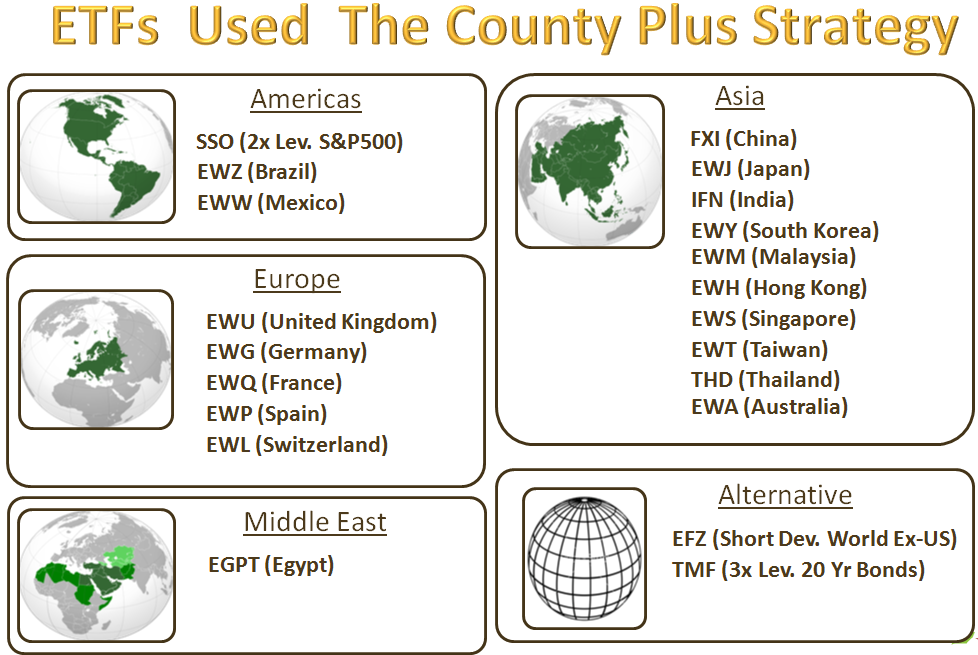

In our country model, we wanted to make sure we had solid diversified geographical representation. We also see the list of countries in our model growing over time as we evaluate and add good country funds as they become available.

Secondly, we wanted our selection of ETFs to be as focused as possible. This point is particularly relevant for the sector model. Many times there were broader ETFs available, but we wanted ones that would move well and pick up on trends quicker than the broader, less specific funds.

Thirdly, we wanted a way to amplify our performance when we are right (and remember this model gets it right a lot more than it gets it wrong). For this we incorporated several leveraged ETFs. They give us the ability to get double or triple the normal performance of holding an unleveraged ETF.

This is one the newest areas of development in the ETF universe and many sectors and most countries don’t have good leveraged products, but where they were available we chose a selection of them to add to model. In the country fund, we specifically included the SSO (2x SPY) so that we could have greater exposure to the U.S. markets when they were trending well.

Finally, we wanted a way for our model to make money even when markets were going down. So we specifically looked at negatively correlated ETFs (ETFs that tend to move in the opposite direction of the broader market). That’s why we included the SDS and treasuries in the sector model and the EFA (short world exposure fund) and the treasuries in the country fund. We will get into greater detail on this point in one of the upcoming strategy emails.

Depending on the specifics of whatever model we are trying to create, the right number and selection of instruments might be quite different. But it is important to remember that this is one of the first key decisions in designing a model. Stay tuned next week as we go over creating rules to avoid buying at the wrong time and how we designed out money management system for the ETF models.

For the sector model, we will continue to hold SOXL, ERX, and DRN. TMF (treasuries) is ranked 4rd and had a good week up 4.38%. It remains the most likely substitution in the model should the markets take a turn for the worse. Stay tuned to the daily updates for any changes.

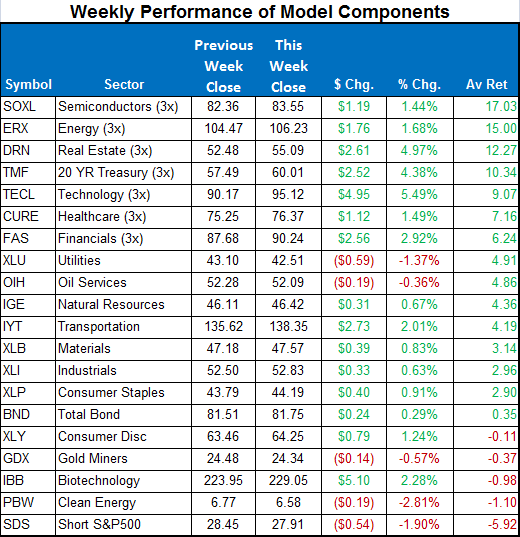

Here is a summary of the weekly performance of all the ETFs that the strategy monitors:

Best wishes for your trading,

James Kimball

Trader & Analyst

MarketGauge