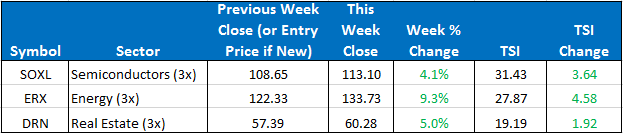

This week there were no position changes in the Sector Plus model. Our current three positions are SOXL, ERX, and DRN. To open next week, we will remain in those three ETFs.

The SPY closed the week up +0.93%. The ETF Sector Plus model had another market-crushing week ending up +6.15%. The ETF Sector Plus Strategy is up +42.83% year-to-date compared to its benchmark, the SPY, which is now up +6.09% year-to-date.

Note to ETF Sector Plus Users:

We are changing the displayed “Av Ret.” to “TSI” which stands for Trend Strength Indicator. The calculation is unchanged. We feel that the new name is more accurately descriptive of what we are trying to measure.

This Week’s Strategy Lesson: Designing A Strategy (Part 7)

We took a short break from this series to talk about some of the changes to the Sector and Country ETF models. The stops and target systems represent an exciting new way to trade the models. We are now going to resume and close out this series. For any of our new members, all the strategy emails are archived on the website if you want to go back and read the previous entries in this series.

Diversification

Modern portfolio theory is one of the guiding principles used in money management industry-wide. It is a quantitative model that attempts to maximize the expected returns of a portfolio for a given level of risk. To actually calculate it requires a lot of high level math and understanding some big words, like “correlation coefficient” and “variance/co-variance matrix.”

While many in the industry argue with some of the results or the idea that you can precisely calculate your level of risk, the fundamental finding of this area of research is not disputed: Diversification lowers the risk of your portfolio.

There are many things that cause this. Individual stocks have unique exposure to event risk. Earnings reports, press releases, and news reports about them and their sector can all drive big moves in a specific stock. Economic reports can move specific sectors or countries while not moving the broad market. A report of conflict overseas could send the whole market tumbling while not budging a small niche stock at all.

To measure these types of effects, financial theorists have developed concepts like beta and correlation. They are imperfect measurements, primarily because they fluctuate, and can be most wrong when you need them to be the most right. During a crises, these values tend to converge on the same value (i.e. in a crisis, stocks will tend to move in the same direction more than during normal market conditions). The one thing we can take from all of this, though, is that with each position you add to your portfolio, you tend to reduce the volatility of your returns.

In each of our models, we have a basic level of diversification built in. We start with using ETFs, which are based on the returns of a basket of stocks. Already we have reduced a lot of the volatility of holding individual stocks. Secondly, we hold three different sector or country ETFs. Not a high level of added diversification, but an incremental improvement.

But there is another step that we can take. We can trade multiple systems. The sector fund tends towards higher returns and higher volatility, while the country fund has lower relative returns and risk. A large part of the difference is the inclusion of more leveraged funds in the Sector model. But we can also expect that sectors will move differently and behave differently than the geographically diverse country holdings.

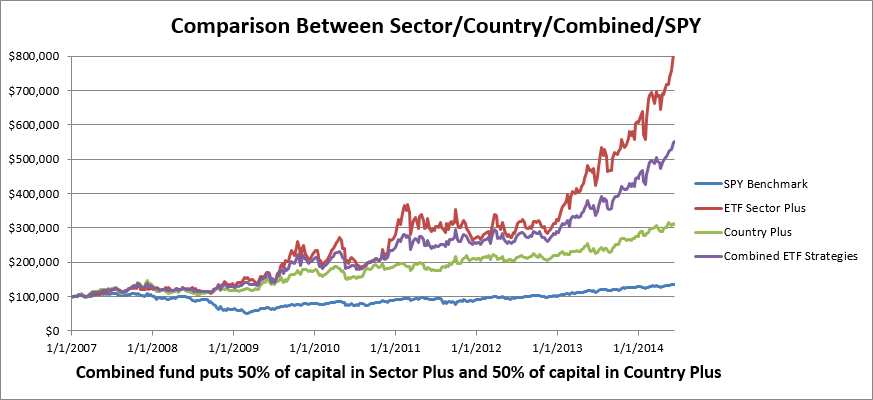

We can take advantage of these differences by creating a hybrid system that trades both strategies, putting 50% of the capital into the three sector holdings and 50% of the capital into the three country holdings.

This will tend to reduce your overall return from just trading whichever one is performing the best, but it will reduce the overall up-down volatility of your portfolio. And over any specific period, we can’t know which one will perform better. During a quick pullback, the more conservative portfolio will outperform.

An interesting thing to note from this example is that by combining these two strategies, you are actually increasing your return on a risk-adjusted basis. Meaning, for each “unit” of risk you are taking, you are getting a little higher return than from each “unit” of risk from trading either individual model. The difference being that you are taking less overall risk, so the return will still be between the results of the two funds.

Without doing the math, you can visualize some of this just looking at the chart below. You can see that the peak-to-trough ranges for the combined model is lower than the sector model… and is only slightly higher than the country fund, while providing a nice improvement in return over just trading the country fund.

Some people on Wall Street call diversification the only “free lunch” in the business. It’s the simplest way to improve your risk/return ratio and continues to be one of the most important things to consider when designing and implementing a strategy.

The Current Condition of the Model

For the Sector model, we remain in SOXL, ERX, and DRN. All three continue to perform outstandingly, sitting on huge gains. CURE has moved into fourth place but is still lagging our top three positions in “TSI” No position changes are imminent in the sector model but stay tuned to the daily updates should there be any changes.

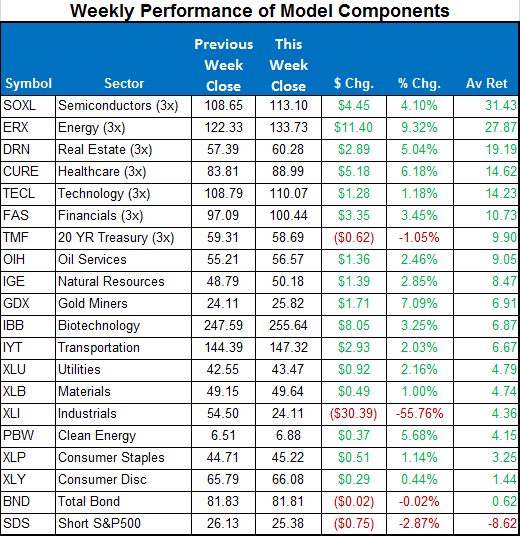

Here is a summary of the weekly performance of all the ETFs that the strategy monitors:

Best wishes for your trading,

James Kimball

Trader & Analyst

MarketGauge