March 16, 2016

Mish's Daily

By Mish Schneider

Think of Banana Split and Licorice

Yesterday, I had two songs in my head. Today, I’m tone deaf. Well, maybe that’s a bit of an exaggeration. I do keep thinking about the post FOMC market volatility while humming to myself, “Take off the gloomy mask of tragedy, It’s not your style..”

Yes indeedy. Our folks at the Federal Reserve, headed up by Janet Yellen, who, although I would have never put this together before, looks oddly enough like Tony Bennett, the lyricist of our song.

Seriously though, after the FOMC comments that possible rate hikes this year have been reduced from 4 to 2 times at most, my “gloomy mask of tragedy” that the S&P 500 was forming the mother of all head and shoulders tops, has caused me to, “Wipe off that full of doubt look.”

Sort of

My hesitation on thinking that all is right in the world again is partly technical, partly fundamental.

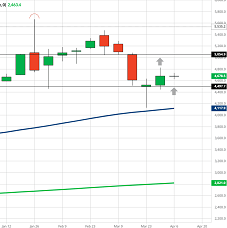

The Head and Shoulders potential top in the SPY still has to clear 204, or what I am calling the breakout zone, which would then make the H&S look more like a humongous double bottom.

However, Wednesday’s high in the SPY was 203.82. Close enough, but no cigars just yet. Volume, although higher than Tuesday’s, sits under the daily average.

The divergences in the Economic Modern Family have me equally incredulous. While sectors such as Semiconductors (SMH) and Transportation (IYT) continue their ascent, other members such as Biotechnology (IBB) and Regional Banks (KRE) struggle to stay afloat.

The Russell 2000 (IWM), even older than Tony Bennett is, performed ok. IWM looks nothing like its daughter Semiconductors though, which is trading well over the 200 DMA.

Granny Retail (XRT), (sorry, I’ve had enough fun with Janet already so will leave this one alone,) had a chance to recapture the 200 DMA and instead closed red.

As I rely on the Economic Modern Family to trade in alignment for the best clarity, these divergences leave me a bit out of key. Which sectors are right and which ones are wrong?

Furthermore, commodities rocketed as well after the announcement.

Gold, Silver, Oil, Coffee, Sugar, to name a few, all had significant gains. The US dollar dropped. Of course the old paradigm that commodities and equities work counter cyclically to one other could be a thing of the past. Nevertheless, I’m not fully convinced of that just yet.

Fundamentally, the strangest Presidential Primary I’ve ever lived through, continues to play out. Although air strikes have had success in wiping out some of ISIS, I’m betting that terrorist threats still loom.

And with the ECB announcing that that was their last time reducing rates, the negative interest rate deck of cards has been dealt.

So while we “spread sunshine all over the place,” and “stick out that noble chin,” I will try not to be a “mean old thing.”

S&P 500 (SPY) 200 key support to hold, 202 pivotal and 204 should bring in more buyers

Russell 2000 (IWM) 105 support, 107 pivotal and over 109 much better position

Dow (DIA) Almost filled the pap to 173.97

Nasdaq (QQQ) Must continue to hold 106 and clear 108.

XLF (Financials) 22.20 support

KRE (Regional Banks) Has to clear 38.50

SMH (Semiconductors) On new 2016 highs

IYT (Transportation) Next up the 200 DMA at 140.88

IBB (Biotechnology) 250 pivotal

XRT (Retail) 45.50 pivotal

IYR (Real Estate) This has not been over 77.21 since it melted down last April.

GLD (Gold Trust) Over 120 again and bears should shut up

SLV (Silver) Will look even better if closes over 15

GDX (Gold Miners) Awesome

USO (US Oil Fund) 9.80-10.00 now support. Over 10.29 should see 10.93

XLE (Energy) 62.00 area now support to hold

TAN (Guggenheim Solar Energy) Cleared 24.30 so now want to see that area hold

TLT (iShares 20+ Year Treasuries) Still in bullish phase

UUP (Dollar Bull) 24.72 recent lows

Every day you'll be prepared to trade with: