November 8, 2015

Mish's Daily

By Mish Schneider

By the end of last week, I was thrilled that the jobs report and increase of 2.5% of hourly wages are positives for the US Economy. However, I continue to feel let down by the Federal Reserve and their capitulation on raising rates or not.

Unless I missed something, as of this writing, no announcement by the Fed has been made. Tons of speculations and odds were tossed around about a December hike. Yet, substantial news? Didn’t see any.

Personally, I wanted Janet and the gang to raise last May when the market was climbing up to new highs. Had they done so months ago, our dialogue (and the market action) would be very different now.

2 weeks ago, I reminisced about 1979 and Paul Volcker’s decisiveness to raise interest rates in order to fight rising inflation.

In 2015, the complexity of the Fed’s decision to raise rates or not comes from exactly the opposite concern-deflation.

The good news? Many of our Economic Modern Family ended on a high note.

The Federal Reserve’s conundrum, besides the rising US dollar, stems from the nearly two trillion dollars of Treasury Bonds and mortgage securities debt they must sell back.

Although raising interest rates will add liquidity to the banking system (why the financial sectors rallied into Friday), it will have negative impacts on Europe and Commodities prices.

Furthermore, the “elephant in the room”, or the 15 Trillion Dollars that the US owes in debt, also gives the FED pause. If the FED raises rates, they will have to pay off the US debt with higher interest rates. Those payments will increase an already bloated Federal Budget.

Nevertheless, my theory is that if they had raised when the Dow traded over 18,000 and while Gold was trading closer to $1170 an ounce, the conversation would be about how Europe came back from a sell off as they continue to ease.

While the SPY sits close to its highs, only about 92 of the S&P 500 stocks are within 3% of their highs. I imagine timelier Fed action would have brought back way more buyers into individual equities (as well as commodities.)

Although it’s easy for me to sit back and play “armchair” economist, time to move on and switch gears.

Economic Modern Family

Granddad Russell 2000s, in particular, closed out the week above the trifecta of resistance.

Regional Banks flew to levels not seen since 2007. Retail, on the other hand, could not close back above its 65-week moving average.

Transportation, not even close to it 65-week MA, rallied into the overhead resistance. Biotechnology could push higher if the others do, but right now, it sits close to its 50 DMA.

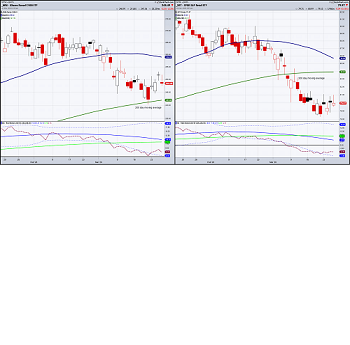

Semiconductors ended back over the 200 DMA. Note that it needs to clear 56.36 to get really interesting.

For this week, continue to focus on the financial sector and the Russell’s. Moreover, equities related to entertainment and leisure along with food will be on my radar.

Finally, food costs which are high, do not reflect the low commodity prices. That anomaly intrigues me. As we approach winter remember-Mother Nature ultimately rules the roost!

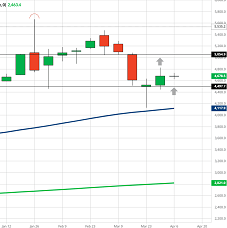

S&P 500 (SPY) 210 remains pivotal with 213 the big area to clear

Russell 2000 (IWM) Cleared the September 17th spike high, the 65 week moving average and the 100 daily moving average, over 119.00. Next week we begin by watching to see that hold

Dow (DIA) 177.70 near term support with 180 the big point to clear

Nasdaq (QQQ) The euphoria will continue if this clears 115.25 area. Runaway gap low is at 112.07

XLF (Financials) Closed the week well with 24.50 area the place to hold

KRE (Regional Banks) I was fooling around when I named this the Prodigal Son. Runaway gap so Friday’s lows important to hold

SMH (Semiconductors) 54.22 the 200 DMA to defend and 56.36 the point to clear.

IYT (Transportation) 148.60 then 150 points to clear with 146 place to hold.

IBB (Biotechnology) Range to break one way or another 320-340

XRT (Retail) Like that this held the 50 DMA. Now, want to see this climb over 46.50 again

IYR (Real Estate) one of the jobs report’s casualties. Landed on the 100 DMA

ITB (US Home Construction) Has spent 5 weeks trading around converging moving averages-big move one way or another coming-26.50-28.00 range to break one way or another

GLD (Gold Trust) On July-August lows. If there were ever a place for this to wake up from-this is it.

SLV (Silver) A break of 14.00 would not look good. However, a move over 14.20 should bring this back to life

USO (US Oil Fund) 14.00 good support level to hold

OIH (Oil Services) 32.00 pivotal

XLE (Energy) 68.50 level a good risk point to hold. Back over 70.00 probably good

XOP (Oil and Gas Exploration) Inside day on the 100 DMA

UNG (US NatGas Fund) Held in a good spot if watching for a long

TAN (Guggenheim Solar Energy) A move over 30.60 would be a good way to start this week

TLT (iShares 20+ Year Treasuries) 118.70 important area to hold

UUP (Dollar Bull) Not quite 2015 highs but close

Every day you'll be prepared to trade with: