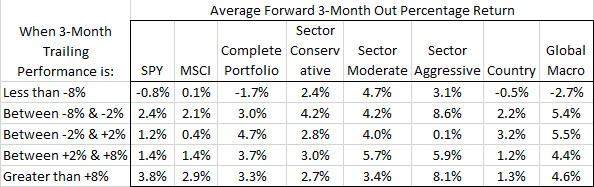

The brackets do not represent equally likely market events. The data looks at the trailing performance for each of the models and the SPY based on their own performance, so each category will have a different number of observations for each model.

However, averaging across them all, the +2% through +8% bracket is the most populous of the brackets with an average of about 30% of the periods falling in this bracket. The greater than +8% bracket is the second highest with 25% of the period, followed by the middle bracket with 20%, the -8% through -2% bracket with 15% and the less than -8% bracket with 10% of the periods.

Looking at the SPY, we see that following a strong negative period, the SPY tends to continue lower, though at a slower pace. Given the extreme category of a -8% move over three months, most of the events in this category happened in 2008 with the financial crisis (about 2/3rd of all -8% or worse periods).

If you excluded the 2008 data from the -8% or worse, where the market took a dive and then continued lower, we see more mean reversion in the data (meaning the tendency for the market to reverse after an extreme move).

Following the strongest periods, the SPY tends to continue higher, though also at a slower pace (mild mean-reversion).

When looking at the models, for average performance across all the models, the -8% through -2% category was the strongest in-terms of forward performance with the +2% through +8% category being the second strongest, although there was not a huge amount of variance for each of the categories with the exclusion of the most extreme down category where follow-up performance was still positive but lagging behind some of the strength in other categories.

The ETF models tend to have their best performance when the market is trending well. This is because a broad positive trend tends to improve the overall win rate of the trades and the higher beta or stronger trending instruments outperform.

Though we also see good performance following a negative period, even when the market doesn’t cooperate. This is because the way the ETF models are constructed and managed, when there is a strong negative market trend, the models will only be in the ETFs will the best absolute positive momentum or be in cash. During these periods, alternative or short ETFs will tend to have the strongest absolute positive momentum. ETFs related to bonds, inverse indexes, and commodities can often perform well in these periods.