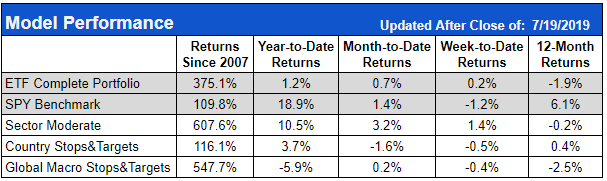

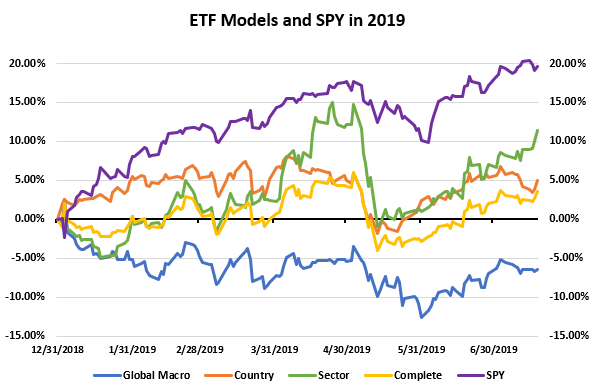

The chart above shows the year-to-date performance of the ETF model and its components. The ETF models have largely lagged behind the S&P 500 due in large part to the timing of the V-bottom hitting just before new years and how those large quick moves and reversals can play out in the ETF models. Though the ETF Complete has marginally outperformed the index from its low in early May.

Unfortunately, the Sector models were hit disproportionately in the May drop due to their heavy allocation in Technology and Semiconductors, two sectors with some of the highest ties to Asia and most effected by the trade talks.

The current holdings of the model are fairly mixed between traditional longs and some alternative holdings. The Sector model currently had Gold Miners and Solar Power, two traditionally alternative holdings, with the third holding in Semiconductors (just rotated into them this week).

The country model is entirely in emerging market countries of Greece, Russia, and Brazil. The Global Macro model is in Solar Power, Water Resources, and just recently rotated into the NASDAQ 100 (QQQ).

This allocation reflects some of the dichotomous nature of the markets right now, just off of all-time highs but significant storm clouds are on the horizon and markets have shown a disturbing lack of resistance to sudden and steep declines.

It will be interesting to see how these holdings and allocations play out or change as the second half of 2019 unfolds.