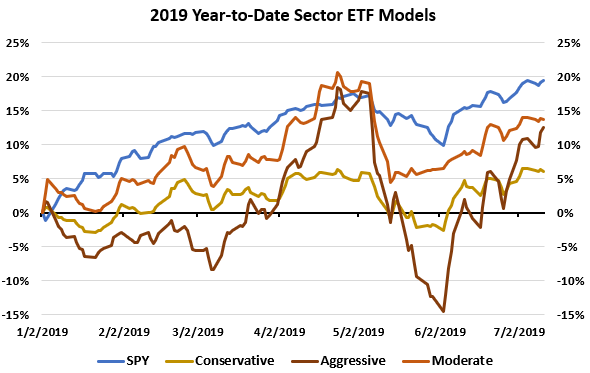

The sector models have had mixed performance so far in 2019. They currently sit between +6% and +15% on the year, though that is lagging a little relative to the index. The models were also coming off their lows to start the year, however, unlike the indexes, the ETF models are still off from their all-time highs in early 2018.

The Sector Conservative model had the lowest volatility, about on par with the index. Both the Aggressive and Moderate model have spent time lagging the index and briefly surpassing it in early May before the recent drop and correction.

The ETF allocations in the Sector portfolios remain mixed. In the Conservative and Moderate, we are in Home Builders, which is a traditional long sector, however, we are also in Gold Miners and Solar Power, which have alternative characteristics. The Aggressive is in Semiconductors and Technology, but also has an allocation into the alternative/rate sensitive Real Estate sector.

Next week we expand our analysis and look at the performance of the ETF Complete and its constituent models.