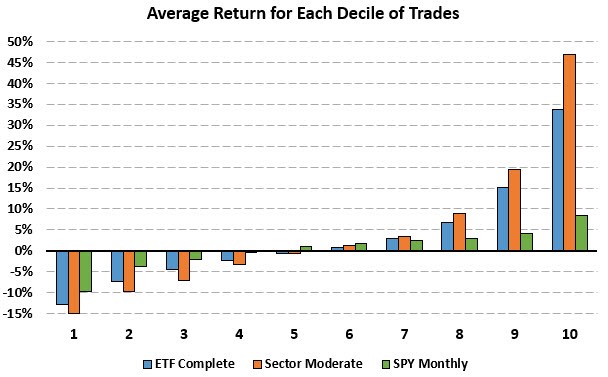

The chart above returns to the probability distribution we looked at last week, but now with the Sector models and the SPY added in. The SPY uses monthly returns instead of trades. It is far from a perfect equivalent but should work fine for our purposes here.

To review, the chart above takes all the trades from each of the models (or monthly returns for the SPY), sorts them by return, separates the trades into 10 equal buckets, and finds the average return for all the trades in each bucket.

One way to look at the chart above is to imagine you were playing a game where you were randomly pulling out marbles from a jar blindfolded. In the jar, there are 10 marbles, each with a different number printed on it corresponding to the 10 average trade return buckets.

Essentially, this marble picking process simulates the potential returns we might get from any one trade chosen randomly. While we would like to get one of the better outcomes, for any one trade, the results could fall anywhere on this spectrum. As our marble or trade sample size increases, we would expect the results to start to look like the chart above.

To convince a normal, rational person to play this game, the game needs to have a “positive expectancy.” At the end of the day, the player needs to know or believe they will be up, whether by winning more often than losing or winning more when you win than lose.

The probability distribution in the chart fits this bill. While it is close to 50/50 on winners versus losers, the magnitude of the difference between the average size of the winning versus losing trades is large at around 2-1. There is some variance, as the Sector model has larger winners and larger losers than the Complete, but the ratio between the size of the average win and the size of the average loss stays about the same.

Understanding the probabilities and outcomes of a model can help us set the right expectations and stick to the rules, both when the model is hitting on all cylinders and when we experience the inevitable pullbacks, knowing that the long-term odds are in our favor.