September 18, 2022

Weekly Market Outlook

By Keith Schneider

I grew up on the shores of Lake Erie. From a very early age my parents enjoyed boating. Their passion grew from a small (24’ wood boat) to larger, pleasure boats (41’) as I got older. Nothing made my late father any happier than being out on the water in his boat.

I grew up on the shores of Lake Erie. From a very early age my parents enjoyed boating. Their passion grew from a small (24’ wood boat) to larger, pleasure boats (41’) as I got older. Nothing made my late father any happier than being out on the water in his boat.

I have such fond memories of being on the boat on nice summer days cruising on the lake with endless sunshine and the wind in my hair. We would go to one of the many islands, Canada, or another fun destination.

However, sometimes the lake was rough, and then it wasn’t much fun. I remember getting sick from being tossed around from the rough seas, because…

Lake Erie is the shallowest of the Great Lakes.

As a result, it can get rough extremely quickly when the wind picks up.

I was on some very harrowing trips when the lake whipped up quickly and the lake grew ferocious by the minute. I recall transitions from calm summer fun to the tumultuous chaos of 6-to-10-foot waves taking only minutes.

These transitions resembled the 2022 stock and bond markets, especially when unfavorable news comes out.

This past week started off with a positive Monday. Then Tuesday’s August CPI (Consumer Price Index) date was released. Instead of the expected pullback in the monthly inflation numbers, the readings were slightly hotter. And the year-over-year inflation numbers stayed elevated at 8.3%.

The expectation was that the decline in energy prices (gasoline) would offset other inflationary prices. Energy has declined but food and rents continued to climb.

After the release of the data early Tuesday morning, the market turned negatively very quickly. Most analysts and market pundits were expecting to see the previous rate hikes begin to soften the rate of inflation. Their thesis was if we saw slower inflation numbers, the Fed would be inclined to pivot and raise rates in a smaller increment next week at their upcoming meeting. With the unexpected new data, all bets are NOW on that the Fed raises by at least 75 bp. Some economists, like Larry Summers (ex-Treasury Secretary) are insisting that the Fed should be even more aggressive and raise as much as 1.0%. That would be unprecedented.

The stock market went on a severe nosedive (worst since June 2020) and interest rates headed towards new highs (the 2 and 5-year US Treasuries hit new highs, the 10-year did not)

The lingering inflation picture is captured below.

Then on Wednesday, the PPI (Producer Price Index), which is the Fed’s more closely watched index, came out and backed up the higher inflation story from the previous day.

More negative news hit Thursday night when Fed Ex conveyed to the world that a major slowdown was occurring worldwide, especially in China and Europe (more on Fed Ex below). Consumer Sentiment also came in disappointing on Friday morning and exacerbated an already dismal week of news.

Fox financial news anchor Charles Payne recently pointed out that if they were still doing the calculations based on the methodology from the 1970s-1980s, inflation would be around 16% right now. However, the government changed the way it calculates these inflation indices by using different weighting. See below:

It was a rough week in the stock and bond markets. The S&P 500 ended down 5.2% from last Friday, the NASDAQ 100 was down 5.8% and the Small Cap (Russell 2000) held up a bit better but still down -4.5%.

Is this the bottom or will we see more selling?

We don’t know, but our indicators have been RISK OFF for several weeks now. Several of our investment strategies (including Mish) are heavily invested in CASH.

Recession Ahead?

As noted above, interest rates have been rising most of the year. In fact, for holders of Fixed Income (“bond”) funds including variations like Preferred Bonds, Convertibles, High Yield, and even Municipal bonds, 2022 has been a negative year. Historically, this is the worst year for what are typically referred to as “conservative” and low risk instruments. The returns range from down -6% to over - 15% for most of these “bond” funds. And for many Americans, these hold a sizable place in their overall portfolio and are supposed to provide the income they rely on. The double-edged sword is that most investors invested in these types of funds are not only losing principal, but the income they produce is less than inflation. Most pension plans are severely underfunded and will not be able to cover their obligations and could default in the next decade.

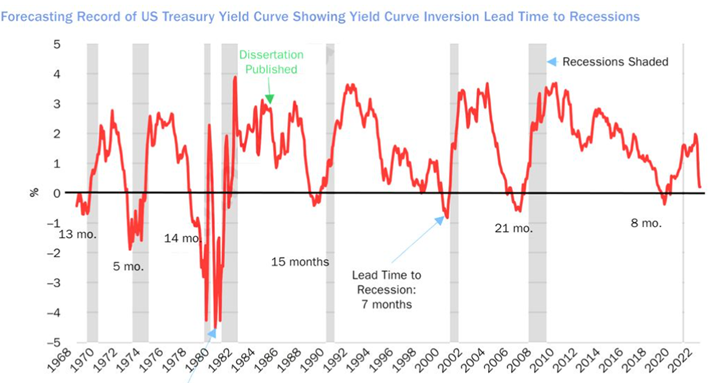

The Federal Reserve watches the yield curve closely. Today the 2-year US Treasury note is yielding approximately 3.78% and the 10-year US Treasury is yielding 3.44%. That means we have an inverted yield curve of approximately -34 basis points. This has ALWAYS forecasted a coming recession. See chart below:

Looking at other areas of the yield curve, we have not seen this big of an inversion between the 2 year and 30-year Treasury Yields since 2000. See below:

Are we already in a recession? Many economists believe so, but if we are not, we suspect we will be soon.

Corporate Earnings are Falling.

In these columns we have frequently discussed earnings contractions coming soon to US companies. This will be due to many factors, these include rising labor costs, health care costs, material costs, transportation, distribution costs and a potential (and real) slowdown of business due to demand destruction and non-affordability factors.

Thursday night Federal Express Corp. (FDX) provided guidance that their business is slowing quite rapidly. They attribute much of their business weakness to China (again shutting down business due to Covid concerns) and Europe, already in a recession. Their concern for a global recession forthcoming (if not already) caused the stock to sell off by 22% on Friday. See chart below.

At the beginning of 2022 Federal Express had a market capitalization of $70 billion and was (and is) a staple of American companies providing important shipping for the supply chain. Today this company is worth $40 billion and has seen 40% of its market capitalization evaporate overnight.

This may be one of many shoes to drop from corporate America. Below is a table of Yardeni Research estimates of earnings the remainder of the year as compared to a large universe Consensus Forecasts:

We want to provide you an easy way to calculate the fair value of the S&P 500 and where this market may go if it factors in these earnings estimates. Please note that a favorable Federal Reserve environment is when they are in an accommodating mode. This means keeping rates lower than inflation or lowering rates. This low cost of capital keeps earnings growing with PE multiples staying on the higher side (18-22x earnings typically).

When the Fed is in a non-accommodative mode, raising short-term rates and/or draining liquidity from the system, we would most likely see a contraction of earnings estimates. In that case, multiples would likely fall to a range from 12-16x earnings, or even much lower during recessions.

The chart above shows the Consensus Estimates of analysts and economists on Wall Street. Ed Yardeni of Yardeni Research does an excellent job of providing his detailed analysis. He shows a much smaller growth projection (3.1%) for the year 2022.

Doing the arithmetic, here are some high-low estimates for the S&P 500 value. Since the market is always looking ahead, this would most likely happen in the next month and certainly prior to the end of the year:

It is safe to say that if there are more companies, like Fed Ex, who will adjust their earnings estimates, we may see the lower side of the above estimates. If, however, we have a soft landing and growth picks up going into 2023, we could see the higher side of the ranges above. The Median of these estimates is about 3600 on the S&P 500 or where we were in June 2022.

Line in the Sand (3900 trend line broken)

This Friday, an important market support line was broken. Many analysts and market pundits have been conveying in their subscriber updates that the S&P at 3900 would likely hold and they felt that was an important point to watch for.

Like a hot knife going thru butter, the market pierced 3900 on Friday and closed below there (and below both the 50- and 200-day moving averages). Notice that support lines below:

Home Buying Is Coming to A Screeching Halt

We have long commented that when housing becomes unaffordable, it will have a dramatic effect on slowing the economy down further. Today, mortgage rates hit the highest they have been at since midmid-2008. Mortgage applications have basically stopped. See chart below:

Affordability in housing is determined by one’s pay (free cash flow), housing prices and the mortgage rates. Given the escalation of housing prices the past few years (up on average 20%-30% in most parts of the country), purchasing a new or upgraded house has become out of reach for many buyers. And as reported in the CPI numbers last Tuesday, rents have gone up to an average price of $2500 suggesting that now people cannot even afford to rent an apartment. This will further affect earnings of housing related companies and force more corporate revisions downward.

Eye of the Storm

A few weeks back we shared with you that September can be a difficult month for the stock market. This is further amplified during midterm voting years. We want to remind you that beginning September 12 through the end of the month, this period can be a very volatile and choppy period.

Was it a coincidence that this past Tuesday (September 13) that the market’s new leg down began?

Please invest carefully during this period. See chart below:

-

5 Actions You Can Take for a Smoother Investment Ride (NOW)!

The best way to utilize our investment strategies is by incorporating a blend that offers disparate investing themes. We have been offering these quant based, algo driven investment strategies through various market cycles and they have held up well. These strategies offer different investment vehicles, from stocks (large or small cap) to various ETFs that provide exposure to stocks and bonds (both long/short), commodities including agriculture, energy (including alternative energy sources) as well as sector specific funds. We know this works and can provide you with an illustration of how blending these together have historically done. We can also do this for you in our Financial Advisory firm MarketGauge Asset Management (MGAM).

If you would like more information on utilizing a “bundled approach” please contact Rob Quinn, our product specialist to discuss several discounted bundles that we are offering under this Smooth Sailing opportunity. He can be reached at (407) 770-7637, or you can schedule a call here:

Here are additional observations from our Big View service:

Neutral

Risk-Off

Every week you'll gain actionable insight with: