The Rotation Continues

US Equity Markets digested recent gains with Grandpa Russell from The Economic Modern Family (IWM) bucking the recent correction in the NASDAQ 100 (QQQ) and the S&P 500 (SPY).

US Equity Markets digested recent gains with Grandpa Russell from The Economic Modern Family (IWM) bucking the recent correction in the NASDAQ 100 (QQQ) and the S&P 500 (SPY).

Leading FAANG+ stocks are losing momentum and ripe for more selling. To us, it appears that there is a combination of sector rotation, changing style bias (Value vs. Growth), and some tax selling taking hold of the markets.

While December, especially mid-month to the New Year has a positive seasonal bias, anything is possible this year. COVID-19 has spiked to its highest levels, and that is still having a dampening business effect in different parts of the country. It may also be creating a negative impact on the market.

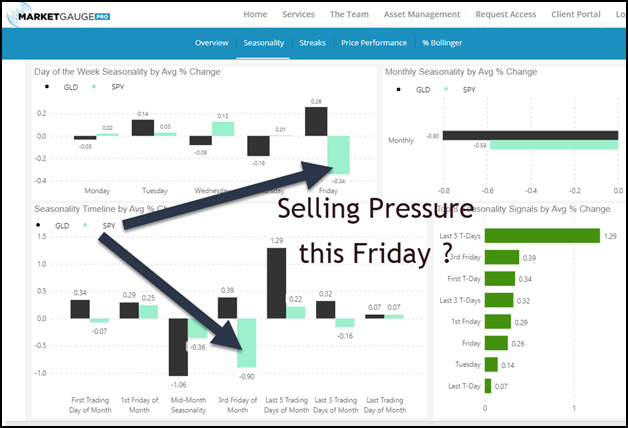

As seen from the dashboard above from the StockOdds engine, next week could see selling pressure in the S&P 500 on Friday. The StockOdds engine calculates the average performance of instruments like the SPY during specific time frames within a specific month (i.e. days of the week)

StockOdds has found that the average return on the SPY on Fridays December is -.34%, and the third Friday (when monthly options expire) has an average return of -.90%.

The highlights of this week’s market action are the following:

- Risk gauges remain in full risk-on mode, although they have weakened overall

- The strength in Small Caps (IWM) +1.1% continued this week, while the other key US equity benchmarks closed down -1% on average

- Volume patterns are still positive for Small Caps while Large Caps (SPY) had zero accumulation days over the past 2 weeks, which is bearish

- Market Internals weakened and are now sitting at neutral levels

- Value Stocks (VTV) continue to hold recent breakout levels versus Growth (VUG). This is where much of the rotation in the market is occurring

- The strongest sector YTD, Semiconductors (SMH +50%) backed off -3.1% last week while Energy, the weakest sector YTD (-31%) gained 1.2%, a rotation that is partially attributable to yearend tax-related trading

- Solar and Clean Energy stocks continue to lead the socially conscious investing surge

- US Long Bonds (TLT) tested recent lows and bounced

- Volatility ($VIX.X) held long term support keeping bearish players a bit more hopeful

- The Yield Curve steepened again, generally a bullish indication for both equities and inflation

- Emerging Markets (EEM) continue to maintain their recent outperformance over US Stocks with Latin America (ILF) leading (one of our current holdings in Complete ETF)

- Energy (XLE), Soft Commodities (DBA) and Minerals and Mining (XME-another one of our holdings) all performed well, suggesting an inflationary environment is underway

- The dollar (UUP)is bouncing off oversold levels short term but is still under pressure

- Gold and Silver also remain under pressure and many traders are finding more opportunities in Bitcoin and recent Initial Public Offerings (IPO’s), which have taken flight and soared to heights indicating a high degree of speculation in the markets

- We are optimistic that the rollout of the COVID-19 vaccines will be successful, and the country and all traders will begin to benefit from a healthier, safer environment that helps usher in a profitable 2021.

If you are a member of Big View Premium or Alpha Rotation, you can find the Market Outlook Premium video here.

Stay One Step Ahead of The Markets and Profit

From The Current Volatility With Market Outlook