May 10, 2026

Weekly Market Outlook

By Geoff Bysshe

Critical minerals are to the digital economy what crude oil was to the industrial economy: a foundational input that quietly powers nearly every strategically important industry.

Artificial intelligence infrastructure, semiconductors, robotics, aerospace, defense systems, electrical grids, battery storage, telecommunications equipment, drones, and next-generation manufacturing all depend on reliable access to critical minerals and rare earth elements.

The national security implications are equally significant.

Rare earth magnets are essential for fighter jets, missile guidance systems, radar, satellites, submarines, advanced communications systems, and AI-related compute infrastructure. In many cases, economically viable substitutes are limited or nonexistent.

As a result, critical minerals are no longer just commodities. They are strategic assets tied directly to technological leadership, economic strength, and military dominance.

Despite the name, rare earth elements are not especially rare geologically.

The real challenge lies in the ability to extract, separate, refine, and manufacture usable materials economically and at scale.

That process is difficult, capital intensive, environmentally sensitive, and technologically complex.

As a result, China currently:

That concentration creates a significant strategic vulnerability for the United States and its allies.

The market received a reminder of that risk in 2025 when China imposed new export restrictions on several rare-earth materials and related technologies following rising geopolitical tensions with the United States.

The strategic vulnerability created by concentrated critical mineral supply chains may eventually resemble the geopolitical leverage historically associated with global oil chokepoints.

Investors are beginning to recognize that securing domestic supply chains may become a national priority rather than simply an industrial policy objective.

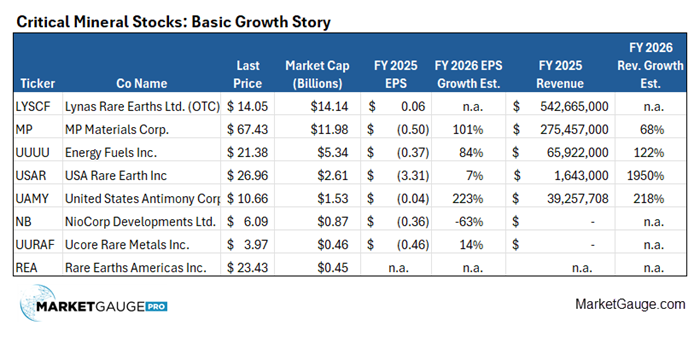

One of the most interesting aspects of this theme is the mismatch between the industry's strategic importance and the current size of the U.S. companies involved.

Many of the companies attempting to build U.S.-aligned critical mineral supply chains remain relatively small, unprofitable, and early in their development cycles.

MP Materials (MP), currently the largest U.S.-based company in the group, has a market capitalization of roughly $12 billion despite operating in an industry tied directly to AI infrastructure and defense systems, where backlogs and budgets that rely on critical minerals are measured in trillions of dollars.

Collectively, several of the major U.S.-related companies tied to the sector represent only about $36 billion in combined market capitalization.

That is remarkably small relative to:

Recent earnings commentary across the technology sector has highlighted enormous projected spending, with backlogs estimated to be over $2 trillion.

It has been estimated that 20 – 50% of the $1.5 trillion defense budget relies on critical minerals as an input.

If investors begin treating critical mineral supply chains as strategic infrastructure rather than speculative commodity businesses, valuation expectations across the group could be rerated.

This potential “expected growth story” appears to be underappreciated by the market.

Many of these companies still have weak earnings profiles, small revenues, and elevated execution risk. That makes technical confirmation particularly important.

Weak fundamentals combined with weak technicals can create substantial downside risk.

However, when market narratives shift, capital flows improve, and technical conditions begin confirming institutional participation, small industries can experience extremely powerful momentum-driven repricing cycles.

Using MarketGauge’s PRIME framework, several stocks in the group are approaching important technical inflection points with improving alignment across price structure, relative strength, institutional accumulation, and momentum.

In particular, several charts are beginning to show:

USA Rare Earth (USAR) currently shows one of the stronger technical configurations in the group, with improving alignment across multiple PRIME factors right below an important breakout level.

MP Materials (MP) remains one of the most strategically important names in the sector. While its shorter-term technical readings have weakened somewhat recently, the longer-term trend structure remains constructive. A successful move through the $73 resistance area could attract renewed institutional participation and potentially signal the next phase of the trend higher.

The AI revolution, rising geopolitical tensions, and increasingly fragmented global trade relationships are accelerating demand, while China maintains an uncomfortable level of control over the extraction, refining, and production of critical minerals necessary for AI infrastructure, defense systems, semiconductors, and advanced manufacturing.

At the same time, U.S. companies attempting to reduce that dependence remain relatively small compared to the scale of the potential demand opportunity in front of them.

That combination can create the conditions for unusually powerful long-term trends:

The market may still be underestimating how important critical minerals could become in the near and long term, and several charts suggest investors are beginning to notice.

If You’d Like To Learn More About MarketGauge Strategies and Systems

If you'd like access to the MarketGauge indicators, strategies, automated trading models, and more, contact us.

Best wishes for your trading,

Geoff Bysshe

Co-Founder

(Connect on LinkedIn)

|

Every week we review the big picture of the market's technical condition as seen through the lens of our Big View data charts. Every week we review the big picture of the market's technical condition as seen through the lens of our Big View data charts.

The bullets provide a quick summary organized by conditions we see as being risk-on, risk-off, or neutral. The video analysis dives deeper. |

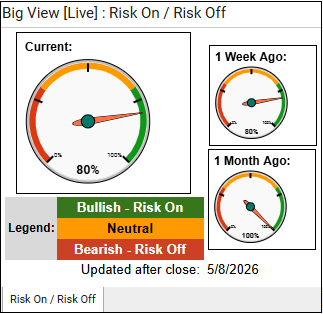

Summary: Markets continued to grind higher this week with the SPY, QQQ, and IWM all pushing to new all-time highs on strong earnings, broad risk-on participation, and subdued volatility, though the Nasdaq is becoming short-term overbought and internals have begun to weaken slightly beneath the surface. Leadership remains concentrated in technology and semiconductors while global equities, growth stocks, and most “Modern Family” sectors stay firmly in bullish phases, although elevated rates, geopolitical risks, and softer breadth suggest the market could be vulnerable to short-term consolidation despite the still-positive intermediate trend.

Risk On

Neutral

Risk-off

The market remains in a strong risk-on environment, so the primary strategy is to stay net long and continue leaning into leadership areas like semiconductors, technology, growth, and small caps while avoiding the temptation to aggressively hedge simply because the indexes are extended. However, with QQQ now overbought on both price and real motion, breadth weakening slightly, and volume no longer overwhelmingly supportive, this is a good time to tighten stops, scale into positions on pullbacks rather than chasing breakouts, and raise some tactical cash into sharp upside extensions.

For now, the tape still favors buying dips over selling strength, but the market is transitioning from an “easy broad thrust” environment into a more selective momentum phase where execution and risk control matter more.

**There will not be a video this week

Every week you'll gain actionable insight with: